Sumber Foto: Indo Premier Sekuritas

Teknologi

GOTO Catat Pertumbuhan EBITDA Positif 21% di 3Q25, Tingkatkan Proyeksi FY25F

Company Update / Consumer Discretionary / GOTO

IJ / Click here for full PDF version

Author(s): Ryan Winipta;Reggie Parengkuan

GOTO

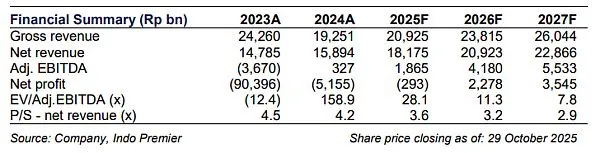

reported Rp516bn positive group adj. EBITDA in 3Q25; 9M25 adj. EBITDA stood at Rp1.3tr (84-95% FY25F guidance; 77% IPS), a beat.

Adj. EBITDA grew by +21% qoq in 3Q25, driven by fintech adj. EBITDA improvement (+55% qoq); while ODS adj. EBITDA was flattish qoq.

GOTO

raised its FY25F adj. EBITDA guidance of Rp1.8-1.9tr; We fine-tuned our FY25F adj. EBITDA forecast by +5%; Maintain Buy rating.

3Q25 pro-forma review: another quarter of adj. EBITDA improvement

GOTO

reported Rp1.3tr positive group adj. EBITDA in 9M25 or 84-95% of its FY25F guidance, a beat against our forecast (77% IPS) and overall market expectation, in our view. In 3Q25, adj. EBITDA grew on qoq (+21% qoq on pro-forma basis) and yoy basis (+239% yoy) to Rp516bn, driven by better adj. EBITDA in fintech (+55% qoq) while ODS adj. EBITDA was relatively flattish qoq at Rp336bn.

GOTO

has also achieved positive adj. pre-tax profit of Rp62bn in 3Q25. Group GTV grew by +6% qoq to Rp176tr, while group net revenues slightly grew by +9% qoq/+21% yoy. Moreover, e-commerce service fee improved to Rp211bn (+6% qoq).

Segmental: tight competition in ODS; fintech continuously grew

For ODS (on-demand services), both mobility and delivery GTV in 3Q25 was relatively flattish with mobility GTV only growing by +3% qoq/+1% yoy, while delivery GTV only grew by +2% qoq/+4% yoy, indicating tight competition in ODS segment. As a result, Adj. EBITDA margin as % of GTV was also flattish qoq at 3.0% for mobility and 1.8% for delivery (Fig. 3). This led to an Adj. EBITDA of Rp336bn (+2% qoq/+115% yoy). Meanwhile, fintech segment's core GTV continuously grew in 3Q25 (+16% qoq/+48% yoy), while outstanding loan also grew to Rp7.6tr (+16% qoq). As a result, fintech net revenue grew by +14% on qoq basis to Rp1.5tr which led to another quarter with positive adj. EBITDA for fintech at Rp136bn (+55% qoq).

Key takeaways from 3Q25 earnings call

GOTO

raised its adj. EBITDA guidance in FY25F from Rp1.4-1.6tr to Rp1.8-1.9tr following the achievement in 9M25. Moreover,

GOTO

has been seeing improvement in GTV growth in Oct25 and overall 4Q25F with 2W mobility segment as the biggest growth driver. On the balance-sheet side,

GOTO

has obtained 4-year loan facility of Rp4.6tr to refinance its previous loan facility; which will be used to support its business and fulfil working-capital needs.

Maintain Buy rating with an unchanged TP of Rp110/share

We fine-tuned our FY25F/26F/27F adj. EBITDA by +5%/+3%/+5%, respectively, and kept our Buy rating with an unchanged SOTP -based target price of Rp110/share. Our Buy rating is underpinned by continuous improvement in Adj. EBITDA along with better GTV growth starting 4Q25F. Downside risks include intensifying competition in ODS.

Sumber : IPS